If you are looking for a community in Edmonton that strikes the perfect balance between nature, family-friendly amenities, and real estate affordability, Kiniski Gardens should be right at the top of your list.

Tucked away in the vibrant Mill Woods sector of Southeast Edmonton, Kiniski Gardens is one of the 26 distinct neighbourhoods that comprise the greater Mill Woods area. With tree-lined streets, exceptional access to the Mill Creek Ravine, and a well-established residential feel, it represents everything home buyers love about mature Edmonton neighbourhoods without the steep price tag found in other areas of the city.

The History and Name: Julia Kiniski, "Big Julie," and the Market Gardens

Kiniski Gardens carries a proud piece of local Edmonton political history. The neighbourhood is named in honour of Julia Kiniski (1899–1969), a Polish-born local reform politician who made a lasting mark on Edmonton City Council.

The Story of Julia Kiniski: Before her eventual victory in 1963, Julia Kiniski ran for city alderman ten times. Her tenacity earned her the affectionate nickname "Big Julie" and reinvigorated public interest in local municipal council meetings. She was only the third woman ever elected to Edmonton City Council, going on to be re-elected three times and leading all council candidates in votes during the 1968 election. She was also the mother of six children, one of whom became professional wrestler Gene Kiniski.

Historical Agricultural Roots: Long before residential construction took off, the southern portion of Kiniski Gardens formed part of the Edmonton Market Gardens in the late 1910s.

The Mill Woods Assembly: The land bank for Mill Woods was assembled by the Government of Alberta starting in 1970, taking its name from Mill Creek and the native Parkland forest trees. By 1971, the City of Edmonton established a formal plan to purchase, subdivide, and sell residential and commercial building lots.

While early development in Kiniski Gardens began in the 1970s (accounting for about 7% of homes), the primary building boom occurred throughout the 1980s (roughly 41%) and 1990s. Kiniski Gardens combines with its neighbour directly to the northwest, Jackson Heights, to form the Burnewood Neighbourhood Area Structure Plan.

Boundaries and Location Context

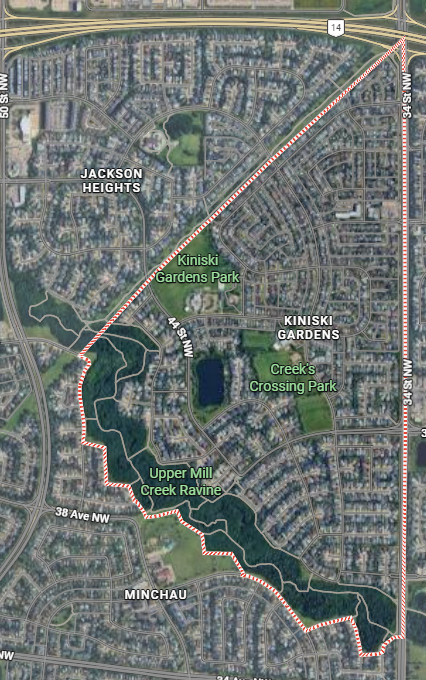

Kiniski Gardens features a distinctive, roughly triangular shape spanning between 1.37 and 1.96 square kilometers. Its clearly defined boundaries give the neighbourhood an insulated, peaceful atmosphere:

Northwest: A pipeline utility corridor running between 34th Street near Whitemud Drive down to the Mill Creek Ravine.

East: 34th Street.

Southwest: The scenic Mill Creek Ravine, which winds southeast and crosses 34th Street.

Features, Parks, and Lifestyle Amenities

What makes Kiniski Gardens such a great place to call home? Simply put: natural beauty and everyday convenience.

Mill Creek Ravine Access: Bordering the neighbourhood along the southwest, the ravine offers residents immediate access to extensive walking trails, biking paths, and natural green spaces.

Kulawy Lake: Situated right within the neighbourhood, Kulawy Lake is a small, man-made lake surrounded by manicured walking paths and peaceful green spaces that enhance the local landscape.

School & Recreational Sites: The focus of the community centers around multipurpose school and park sites. Local educational options include Julia Kiniski Elementary School (Edmonton Public) and Saint Kateri Catholic Elementary School.

Community Leagues: Local recreation and social events are supported by the Burnewood Community League and Woodvale Community League, offering community halls, sports programs, and outdoor skating rinks.

Commercial Convenience: Residents are served by businesses on local commercial sites along 34th Street and 50th Street, while major retail destinations like Mill Woods Town Centre and RioCan Meadows are just minutes away.

Core Demographics: Who Lives Here?

With a population of approximately 5,600 to 6,600 residents living across roughly 2,000 to 2,200 dwellings, Kiniski Gardens is a calm, mature, and family-centric community.

Structure Types: Single-detached homes represent the dominant residential structure, making up between 70% and 95% of total housing units. The remaining properties consist of semi-detached duplexes, row houses, and low-rise apartment condominiums.

High Homeownership: Approximately 85% to 89% of homes in Kiniski Gardens are owner-occupied, pointing to strong neighbourhood stability and pride of ownership.

Family Profile: The community heavily attracts young families, long-time owners, and buyers looking for traditional 1980s and 1990s layouts—often featuring wood-burning fireplaces, pie-shaped cul-de-sac lots, attached or double detached garages, and fully finished basements.

2026 Real Estate Market Context: Kiniski Gardens vs. Edmonton Average

If you are evaluating home options in 2026, Kiniski Gardens stands out as a compelling value opportunity.

Across the Greater Edmonton Area in mid-2026, real estate activity remains solid with increased listing inventory giving buyers plenty of selection. The average price for a single-family detached home in Edmonton sits at $592,989, with overall residential sales across all categories averaging around $483,600.

By contrast, Kiniski Gardens offers a noticeable pocket of affordability. Single-family detached homes in Kiniski Gardens frequently list and sell in the $320,000 to $460,000 range depending on lot size, garage configuration, and overall finish level. Average list prices in the surrounding zone sit around $462,400.

For first-time buyers and growing families, this represents a 20% to 30% savings compared to the citywide average for a single-detached home. You get the benefits of a detached property, private yard, and garage without stretching your pre-approval to the limit.

Why Kiniski Gardens Makes a Great Place to Purchase Property

Equity Building Opportunity: Buying in at an accessible price point allows homeowners to build renovation equity over time through modern cosmetic updates.

Quiet, Low-Traffic Streets: Thanks to its triangular layout bounded by natural features and utility corridors, Kiniski Gardens experiences minimal cut-through vehicle traffic.

Unbeatable Nature Integration: Having both Kulawy Lake and the Mill Creek Ravine in your immediate neighbourhood provides immediate access to scenic walking and cycling paths.

Convenient Transportation Links: Quick connections via 34th Street, 50th Street, Whitemud Drive, and the Anthony Henday Ring Road make commuting to downtown or surrounding industrial parks simple.

Frequently Asked Questions (FAQ)

Q: Where does Kiniski Gardens get its name?

A: The neighbourhood is named after Julia Kiniski, a dedicated local reform politician who was elected to Edmonton City Council in 1963 as only the third woman to ever hold a council seat. Known as "Big Julie," her civic engagement reinvigorated public interest in local government.

Q: What types of homes are in Kiniski Gardens?

A: The vast majority of properties are single-family detached homes built in the 1980s and 1990s. The area also offers a select mix of duplexes, townhomes, and low-rise apartment condos.

Q: What natural parks and amenities are located in Kiniski Gardens?

A: Residents enjoy direct access to the Mill Creek Ravine along the southwest border and Kulawy Lake, a man-made lake featuring paved walking paths and green spaces.

Q: How do single-detached home prices in Kiniski Gardens compare to the Edmonton average?

A: In mid-2026, the citywide average price for a detached home in Edmonton is $592,989. In Kiniski Gardens, detached homes generally range between $320,000 and $460,000, offering buyers a substantial price advantage.

Q: Are there schools within the neighbourhood boundaries?

A: Yes, Kiniski Gardens is home to Julia Kiniski Elementary School (Edmonton Public) and Saint Kateri Catholic Elementary School.

Ready to Explore Kiniski Gardens Real Estate?

Whether you are looking to buy your first single-family home, relocate closer to nature, or invest in a stable Edmonton neighbourhood, Kiniski Gardens offers an incredible combination of lifestyle and real estate value.

Get in touch today to discuss current listings, market dynamics, and how to find the right property for your goals!

Phone / Text: 780-232-2064

Email: mike@pabianrealty.ca

Website: pabianrealty.ca

Mike Pabian | RE/MAX Excellence | 5607 199 St NW #201, Edmonton, AB